PDF Solutions (PDFS): The Orchestration Engine of the $1T Semiconductor Era

Why PDF Solutions is becoming the neutral infrastructure layer of semiconductor manufacturing

In this article, we will look at how a company that has been around for more than three decades, and was once valued like a low-multiple (3-4x sales) niche software business, could be turning into a much more important player: the data and orchestration layer connecting a huge and increasingly complex semiconductor supply chain.

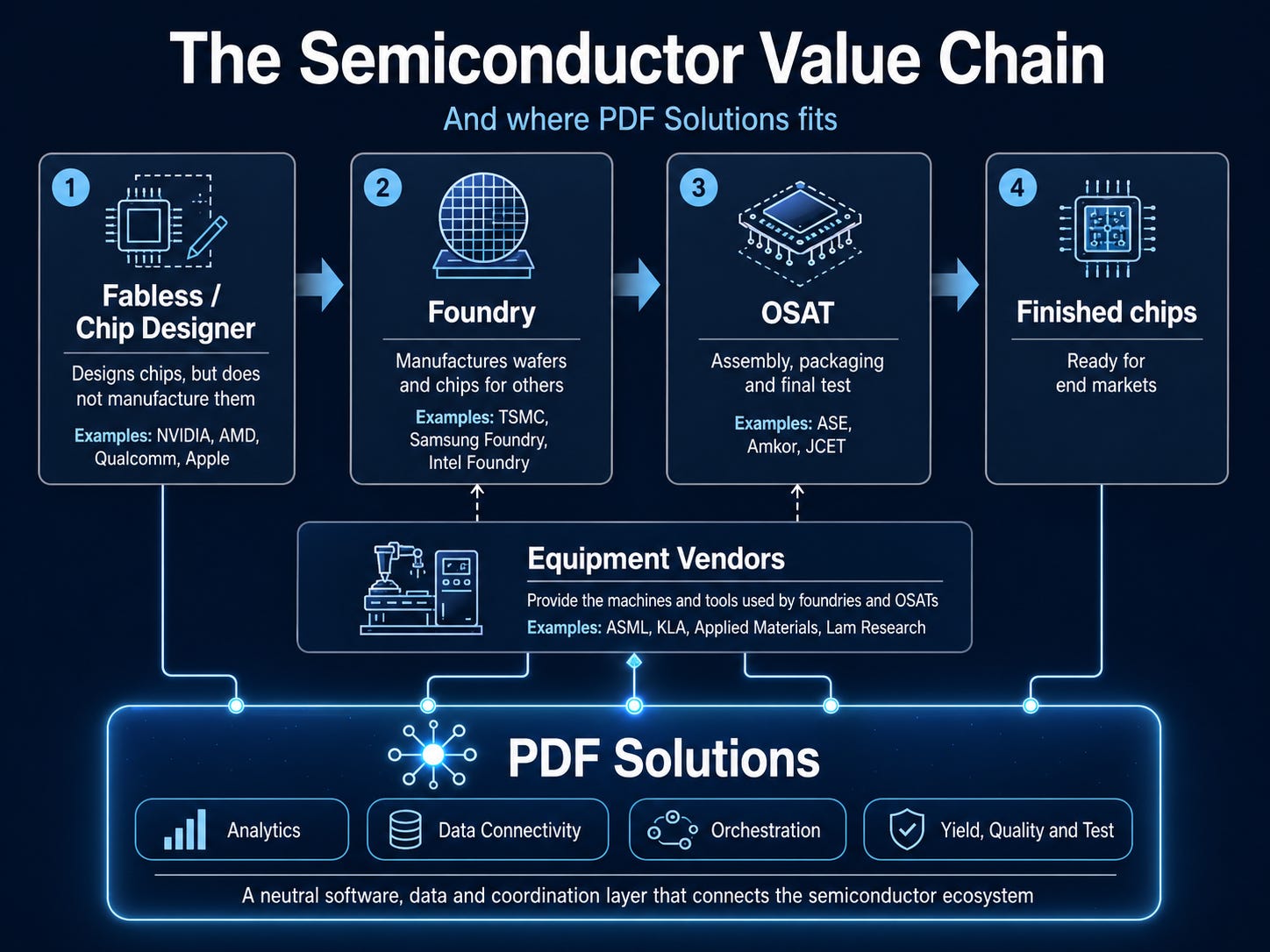

Founded in 1991, PDF Solutions first grew as an analytics platform provider, but the company is evolving toward AI-driven collaboration and orchestration across the fabless (design house), the foundry (the wafer manufacturer), OSAT (assembly operation) and the test operation generate compatible data and share it in real time. That coordination didn't exist. Today it's the industry's bottleneck.

Table of contents.

The Setup

The Sector and the TAM

What the Company actually does

What the Market is Missing

Moat

The Financials

Valuations

Risks

Catalysts

Conclusion

1. The Setup

The semiconductor industry is on its way to becoming a $1 trillion market by 2030, but making chips is getting much harder. As Moore’s Law slows, the industry is moving toward more complex 3D designs and chiplet-based architectures.

In the past, yield analytics was mostly a tool used to study problems after they happened. It sat on top of the manufacturing process rather than being part of it.

Today, PDF Solutions is trying to become something more important: a core data and coordination layer for the semiconductor industry. As chip manufacturing becomes more global and more fragmented across different companies and production steps, PDF Solutions is positioning itself as the neutral platform that helps connect the whole ecosystem:

PDFS does not design or manufacture chips; it provides the software and connectivity that allows the four primary tiers of the industry to collaborate without compromising intellectual property:

Fabless (e.g., NVIDIA, AMD): Needs to know if their complex 3D designs are manufacturable.

Foundry (e.g., TSMC, Samsung): Needs to ramp up new nodes (2nm) faster and reduce waste.

OSAT (e.g., ASE, Amkor): Needs full traceability from the final package back to the original wafer.

Equipment Vendors (e.g., ASML, Applied Materials): Needs to monitor their multi-million dollar tools inside remote fabs.

The Paradigm Shift: PDFS is moving from being a tool used by one of these players to being the orchestration platform that links all of them.

That’s what explains the sharp recent move this week. And it’s also why the valuation exercise in this deep dive is harder than for a typical software company.

We’re valuing a business-model transition happening in real time.

The companies above are illustrative examples of each tier, not confirmed PDF customers.

2. The sector and the TAM

The reason PDF matters now is that semiconductor manufacturing is getting harder faster than most people appreciate. Management frames the shift around three forces: more 3D structures, a more complex global supply chain, and the need to apply AI across design, manufacturing, test, and packaging.

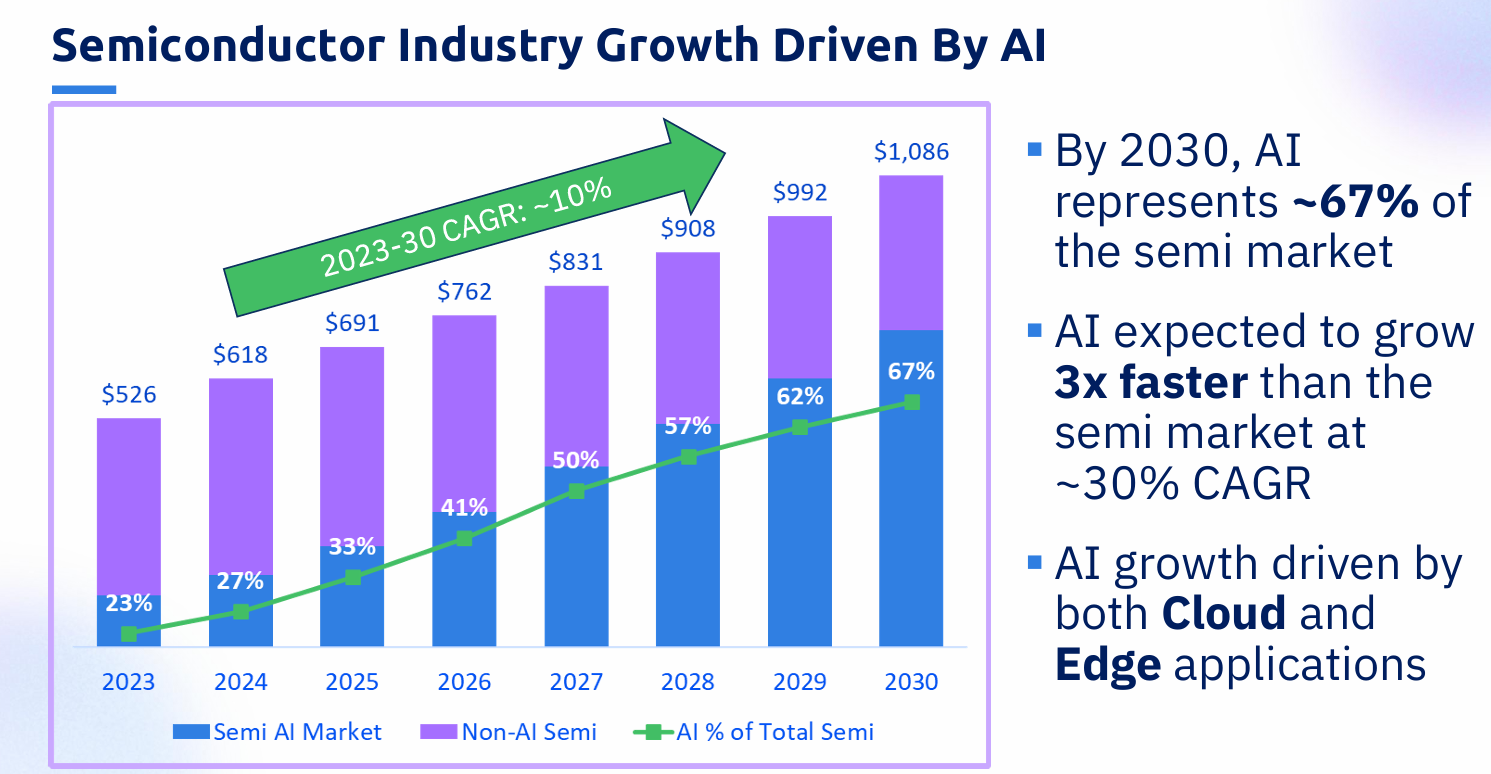

The industry is not just getting bigger. It is getting harder to coordinate. That is the part that matters for PDF. Management’s investor deck says the semiconductor market could reach roughly $1.1 trillion by 2030, with AI representing about 67% of that market and growing about 3x faster than the broader semiconductor market.

The same deck sizes the sub-2nm foundry market at about $100 billion by 2030 and advanced packaging at about $80 billion.

Even if you haircut those numbers, the message is the same: as AI systems get larger, more heterogeneous, and more packaging intensive, the value of data infrastructure, process control, and cross-company coordination rises.

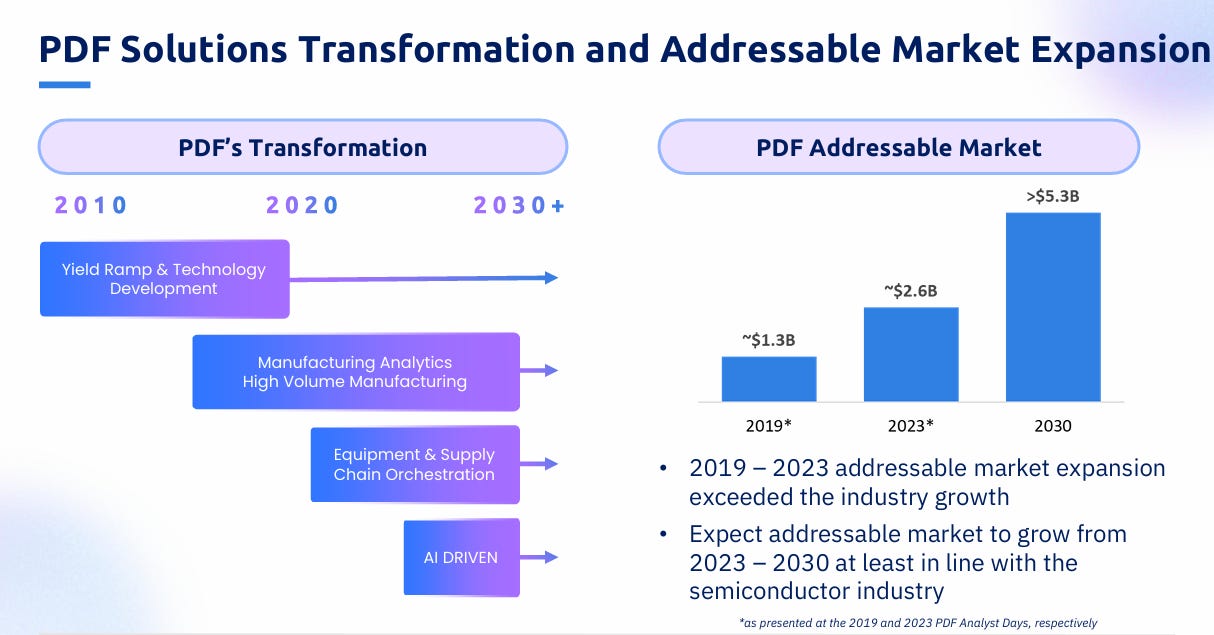

The addressable market history in the deck is more useful than the headline TAM. Management says PDF’s addressable market expanded from about $1.3 billion in 2019 to about $2.6 billion in 2023 and could reach about $5.3 billion by 2030 as the company moves from yield ramp into manufacturing analytics, high-volume manufacturing, equipment and supply-chain orchestration, and AI-driven workflows.

There is also an adjacent market angle: The company website now highlights Exensio Battery, which applies the same analytics stack to battery cell manufacturing. It is not part of the core thesis today, but it is a credible adjacent option because it reuses the same core capability: messy industrial data, process variability, and yield improvement.

3. What the company actually does

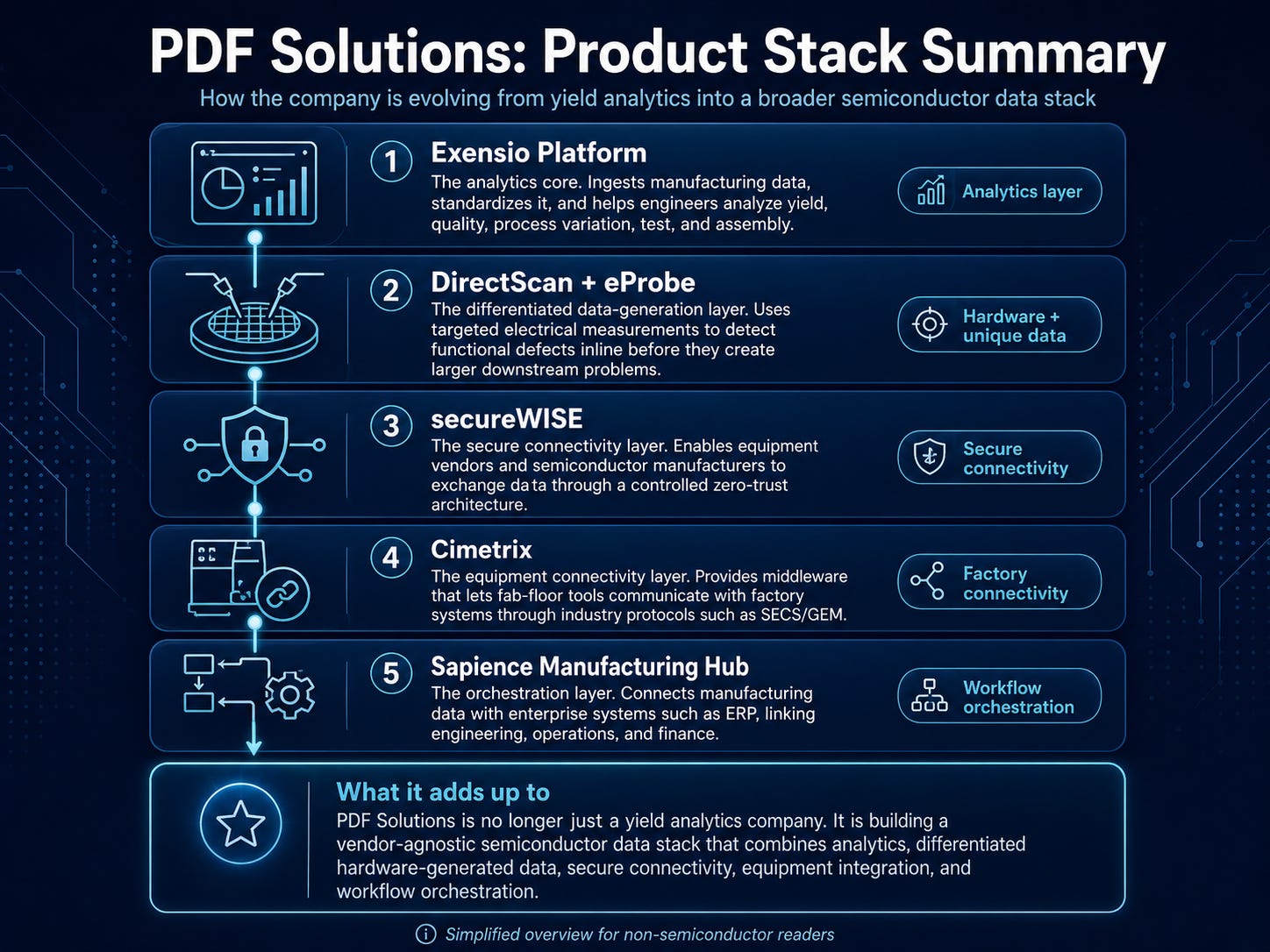

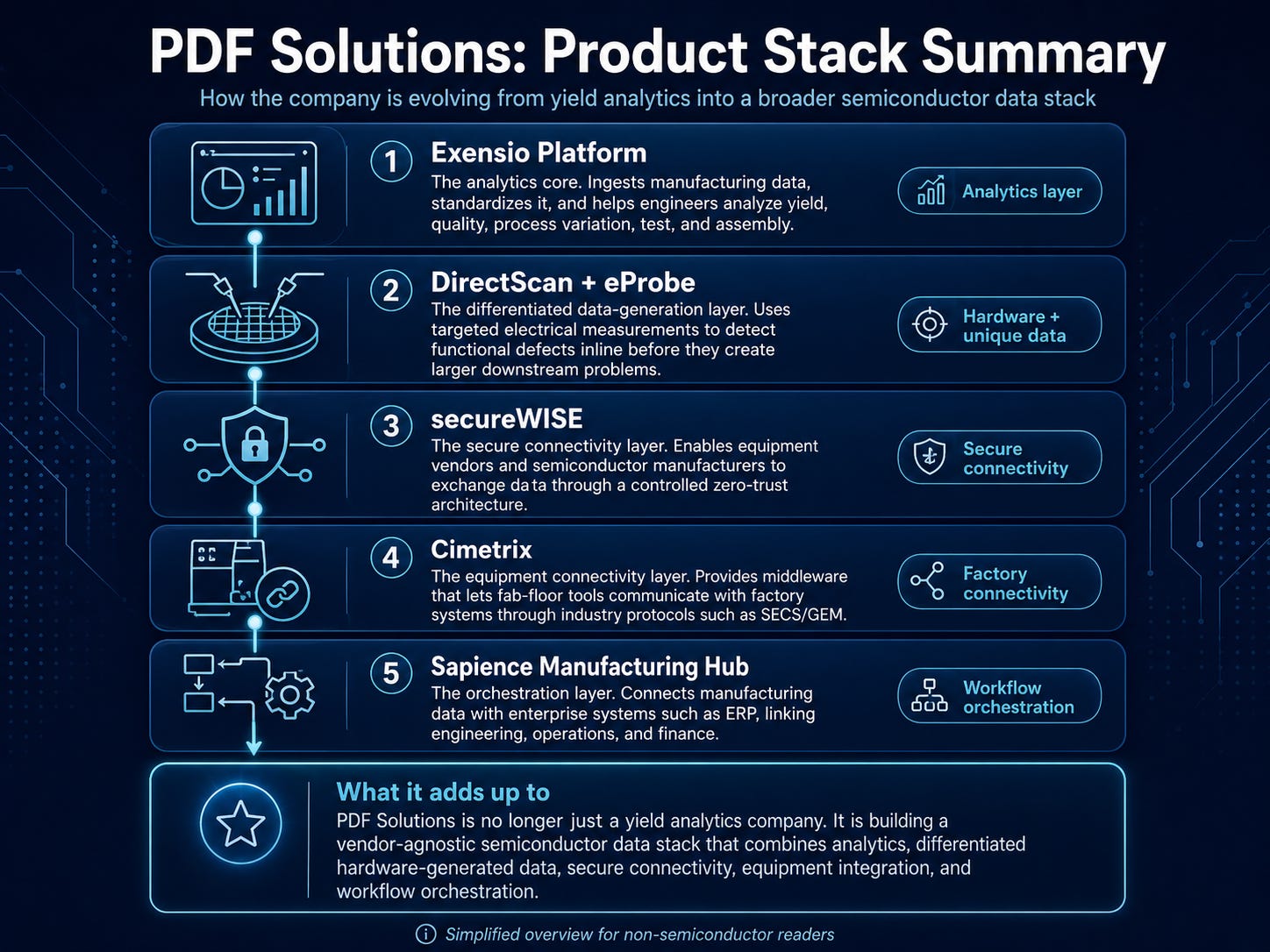

The product stack is easier to understand if you stop thinking about PDF Solutions as a single software product and instead view it as a semiconductor data stack. Each layer solves a different part of the manufacturing problem.

Exensio Platform is the analytics core. It ingests large volumes of manufacturing data, standardizes it, and helps engineers identify yield loss, quality issues, and process variation across fabs, test, and assembly. The simplest way to think about it is as a semiconductor-specific data and analytics platform.

DirectScan and eProbe are the differentiated data-generation layer and the main hardware piece of the story. Instead of scanning full images, eProbe takes targeted electrical measurements on the wafer, allowing customers to detect certain functional defects inline before they create larger downstream problems. Strategically, this matters because PDF is generating valuable proprietary data, not just analyzing third-party data, and management is increasingly shifting the model toward subscriptions and leases.

SecureWISE is the secure connectivity layer. It allows equipment vendors and semiconductor manufacturers to exchange data through a zero-trust architecture. Its importance is that it moves PDF beyond analytics and into governing how data flows across the semiconductor ecosystem.

Cimetrix is the equipment connectivity layer. It lets manufacturing machines communicate with the factory’s central systems. It is not flashy, but it is deeply embedded in day-to-day fab operations.

Sapience Manufacturing Hub is the orchestration layer. It connects manufacturing data with enterprise systems like ERP, linking engineering, operations, and finance. The key value is that it helps customers move from isolated analytics to coordinated decision-making across the business.

Taken together, PDF Solutions is no longer just a yield analytics company. It is building a broader semiconductor data stack that combines analytics, differentiated hardware-generated data, secure connectivity, equipment integration, and workflow orchestration. The strategic appeal is that this stack is vendor-agnostic. PDF does not need to own the fab, the tool, or the ERP system. It just needs to become the neutral layer that helps all of them work together more effectively.

So far, we have covered the setup, the market, and the business model.

From here, we get into the part that really matters: what the market is still missing, where the moat is real or overstated, the key catalysts and risks, the numbers, and the valuation models.